Before my husband and I bought our current home, my goal was to maintain a credit score of at least 720 to qualify for a better interest rate on our home loan. Our lender told us applicants with a 720 or higher credit score qualified for better rates.

So you can imagine my panic when the lender ran my credit and my score dropped to 719!!! My lender calmed me down and said as long as we kept paying down our debt and avoided using our credit cards – our scores should continue to increase before we needed to lock in an interest rate.

I took her advice and kept paying down debt. In the end, we qualified for a great interest rate by the time the builder finished our home.

But then I got to thinking is it possible to increase your credit score and still have some debt? I decided to try an experiment. I’d strive for a spot in the 800 credit score club with some balances on my credit cards.

Spoiler alert: I can confidently say, “Yes.” You can have a high credit score and debt. However, the key to having both requires balance. I am not encouraging anyone to keep debt, but I’m going to show how you can have some debt and a high credit score. Below is information to help you better understand credit scores and tips to improve your own score.

Increasing your score takes time. It took me about a year to reach the 800 range, but it can be done. If your score is not in the 700s, don’t fret. This advice can help you too! Stay focused on improving your score and making sound financial decisions along the way.

What’s a Credit Score?

A credit score is an indicator that lenders use to determine your creditworthiness. It’s actually a predictor of how likely you are to be ninety days or more late on your payments at some time in the future. So, the higher your score, the less likely you are to default on a loan.

A FICO score, created by the Fair Isaac Corporation, is a particular credit score. It’s the most widely used credit score and can range from 300 to 850. Your FICO score is based on all of your credit data compiled by the three major credit bureaus–TransUnion, Equifax, and Experian.

These credit bureaus collect data about the age of your credit history, your payment history, credit activity, and types of debt (think credit cards, mortgages, student loans). They use this information to generate your credit score. You could have different scores at each bureau if one has information the others do not have in their records.

Factors that Affect Your Score

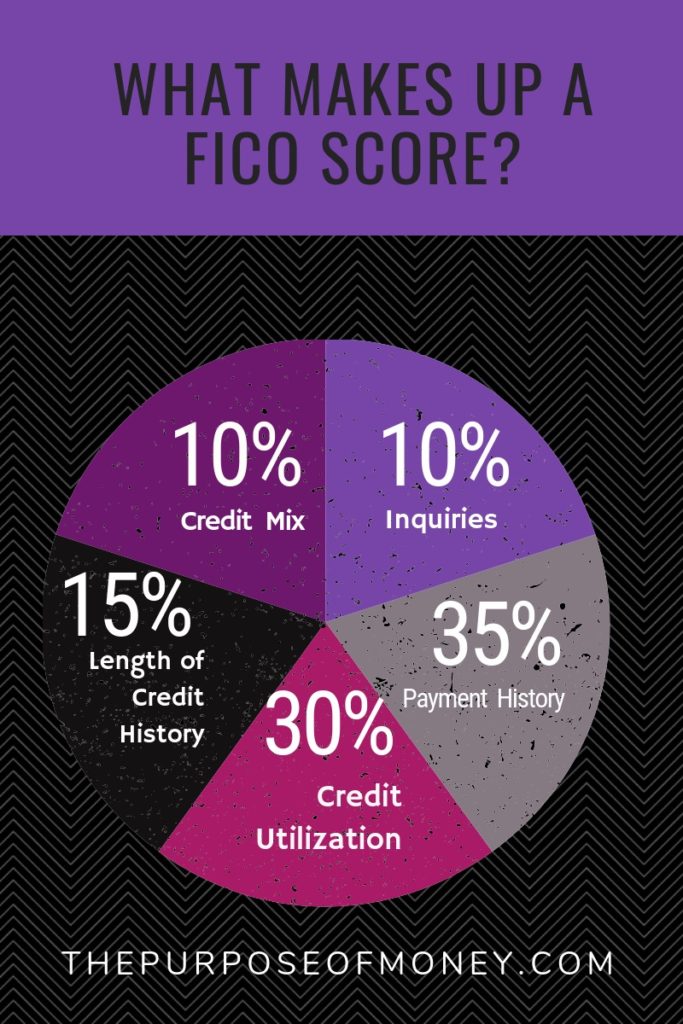

There are many factors that can affect your FICO score but five are the most common. Of the five, the two most important factors are your payment history and the amount you owe. They have the greatest impact on your credit score. But the other factors matter too.

The five factors are:

- Payment history, 35%

- Amount you owe: 30%

- Length of credit history: 15%

- New credit opened: 10%

- Types of credit you have: 10%

Payment History

Your FICO credit score is heavily based on your payment history. Lenders assume that if you made your payments on time (and “as agreed”) in the past, you’re more likely to continue to pay them that way in the future. So you’re a good bet, so to speak – and they’re willing to lend you money.

Delinquent payments have the greatest impact on your credit score. One missed payment could impact your credit score for the next 24-36 months. A missed payment is called “derogatory credit” and, typically, your credit score will improve every 12 months after your last derogatory ‘event.’ I say typically because other things can block the improvement of your score – like increasing credit card balances, a new credit card, or a new loan.

The best policy is to pay your bills on time. So, if a bill payment date falls before you get paid, ask your lender if you can change the bill’s due date. And, if something happens outside of your control – contact your credit card company or lender and let them know what’s happening and that you’re going to be late or miss a payment – before its due.

Amount You Owe

When reviewing your credit report, lenders pay close attention to how much credit you have access to versus how much you’re using at the time. Lenders prefer to see you have access to a lot of credit but are only using a small portion of it. If it appears that you are using credit to live, you may not be approved for more credit.

A good rule of thumb is not to use more than 30 percent of your available credit. For example, if you have one credit card with a $1,000 credit limit keep your balance under $300.

Length of Credit History

How long you have had a credit card can help boost your credit score. The longer you have a positive relationship with a credit card company the better. I got my first credit card in college, and I still have that credit card today–over 15 years later. It’s a good idea to keep your older credit cards open, using them every 6-9 months and then paying them off.

Credit Mix

Just like it’s good to diversify your investments and income streams, it’s a good idea to diversify your debt too. On your credit report, your debt can fall into two categories–installment loans or revolving accounts.

Revolving accounts are credit cards from your favorite retail store, gas station, or bank. The amount you can borrow fluctuates depending on your available credit and outstanding purchases. As long as you keep up with your credit card payments, you can continue to have access to this credit.

Installment loans include auto loans, student loans, personal loans, and mortgages. You borrow a specific amount up front and then pay it back over time. Once you pay off the balance that loan is marked paid in full.

It’s best to have a balance of both installment loans and revolving credit. The installment loans help you build a consistent payment history. Whereas, the revolving credit when paid back, shows you can responsibly borrow money and pay it back.

New Credit Opened

Every time you apply for a loan or new credit card your lender runs your credit. This review will impact your score. Therefore, it’s best to limit new inquiries to one or two total in a two-year span. Too many inquiries will make it seem like you are desperate for credit and will raise questions for lenders. Too many inquiries and denials for credit is also not good, so apply for new credit wisely.

If you do get new credit, before you have a history of making the payments on time – your score will go down. Until you make 6 to 12 months of payments on the new revolving or installment loan, proving you can handle the new debt, your score almost assumes you can’t handle it. But, once you have a history of making the payments as agreed, your score will improve again.

Here’s What I Did

To boost my score over 720 here are the steps I took to balance my credit score and existing debt.

Paid Off Debt

The first thing I did was pay off my car and student loans prior to closing on my current home.

I did this because the lender insisted I lower my debt to income ratio before buying our home in order to qualify. We started clipping coupons and eating out less. You would be surprised but every extra dollar we saved went directly to paying off my loans.

This action alone lowered the total amount of debt owed and at the same time improved my payment history. I paid two loans off in full before getting a home loan.

Diversified My Credit

Purchasing a home helped change my credit mix. Before becoming a homeowner, I only had student loans, credit cards, and a car loan on my credit report. So getting a home loan helped add a new installment loan for real estate to my credit report –which lenders like to see.

If you have a choice between buying a car first or buying a house–get the house first.

Paid My Bills On Time

Over the last seven years, I’ve paid all my bills on time. When we moved into our home, our bills changed. To help keep track of the companies and bill due dates I put every household bill on my phone’s calendar and set reminder alerts.

Although many of my bills are on auto pay, I still use the alerts to remind me to check the bank and make sure all my payments were made. Mistakes happen, and it’s important to trust but verify that your bank’s bill pay system paid your bills.

The only bills I do not auto pay are utility bills. You want to check utility bills every month to confirm your bill is in line with your family’s normal usage. Any spikes could signify meter reading errors, a leak, or some other issue and should be reported immediately.

Said No to New Debt

Since my home loan was approved, I have not applied for any new credit cards or allowed anyone to run my credit. If I was to apply for a new credit card or loan today, the inquiry would impact my score. So until I really need another loan or credit card, I am not applying for one.

My car is about 10 years old and paid in full. It still runs well, but I’m saving now for the next car so we can hopefully pay for it with cash. I don’t want any more car loans. I still have two credit cards but the balance for both is less than $5,000. Both cards are on auto pay and will be paid off by the end of this year. Today, my credit utilization is reduced to five percent of what I could borrow on my credit cards.

You Can Do It Too

Trust me, you can increase your credit score if you follow my steps. As with most things in life, it’s all about balance. If you don’t have a budget you can start one using this template. Then find a way to cut your existing expenses so you can put more income towards debt.

Track your spending and aim to spend less than you earn. If you are having trouble paying your bills, contact your creditor. Either work out a payment plan or request a new payment date that is more in line with your paycheck schedule.

If you cannot repair your credit with time and consistent payments, consider working with a nonprofit organization to repair your credit. Check with your bank or credit union to see if they have any programs that can help you for free before you pay for help.

As you progress along your journey celebrate milestones, such as paying off a credit card or increasing your score. You can track your credit score for free with Credit Karma or Credit Sesame. Checking your own score won’t impact your credit score. Also, many credit card companies or banks, allow you to see your score for free and provide you tips on how to boost your credit score as well.

One thing to note: there’s a difference between the score you’ll see using a consumer credit reporting service (Credit Karma, Credit Sesame) and what a mortgage lender (or auto lender) will see. The reason is that the credit bureaus created a “Consumer Credit Score” which uses a different calculation than the one prepared for mortgage or auto lenders. There’s no actual data on how much lower your consumer score will be, but your best bet is to estimate a consumer score might be 15 to 50 points lower than a lenders score.

Do you have any other credit score tips and tricks? Please share them with the Purpose of Money Community in a comment below.

Click here for more tips to boost your credit score!